Yahoo Finanza

Yahoo Finanza China’s Recovery Stuttering as the Dollar Breaks ¥7

Dollar-yuan closed above ¥7 on 17 May for the first time in 2023 and reached a fresh six-month high the next day above ¥7.05. Various Chinese data this month have come in weaker than expected, suggesting that monetary and fiscal stimulus might be required to boost the economy. However, indices and Hong Kong and China have generally held steady, supported by tech shares. This article summarises the important releases from recent weeks and looks at the charts of USDCNH and HK50.

Strong purchasing managers’ indices from China, both generally and for manufacturing specifically, drove the narrative of recovery in 2023 so far:

In February and March, the data beat expectations and showed growth above 50. However, the figure for April missed the consensus by 0.8% at 49.5%, indicating contraction. Although sentiment remains generally good, there are concerns about both a general economic slowdown around the world and specifically a weaker property market in China.

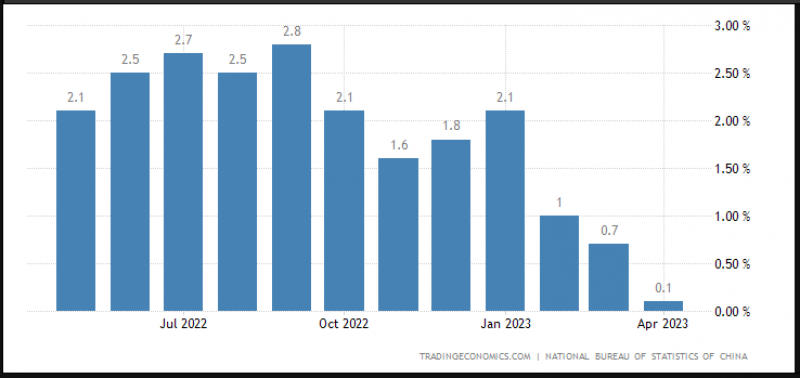

Inflation in China has also reached a significant low after dropping fairly consistently since last year:

0.1% in April was the lowest in more than two years and would usually suggest the possibility of dovish policy by the PBoC to bring the figure closer to 2%.

Earlier this week, Chinese annual industrial production in April was announced to have increased 5.6%, higher than the reading for March of 3.9% but significantly lower than the expectation of around 10.9%. China’s balance of trade has mostly remained stable at around $90 billion in recent months although the value of imports has declined somewhat.

Overall, recent data from China point to a more challenging domestic recovery than might have been expected earlier this year. That’s not necessarily a problem for shares, with the tech sector seemingly likely to continue growth this year and driven primarily by exports, but the offshore yuan might face continuing headwinds in the next few months.

Dollar-offshore Yuan, Daily

Dollar-yuan has moved past the important psychological area of ¥7 for now and seems likely to continue higher in the medium term based on TA. Apart from Chinese news as noted above, fundamental drivers include the continuing hawkish picture for the Fed relative to earlier expectations: there is no confirmation of a pivot by the FOMC and it’s still possible that rates could go higher.

The current leg up by USDCNH still hasn’t clearly broken through the 23.6% weekly Fibonacci retracement, so that combined with a strong overbought signal from the slow stochastic might signal a retracement lower. The 200 SMA around ¥6.976 could be an important support in the short term and the 38.2% Fibo might support the price further ahead.

After Jerome Powell’s comments on Friday 19 May, next week the focus is on American income and spending plus personal consumption expenditures. The PBoC meets early on Monday morning GMT but a change to either the annual or five-year loan prime rate seems unlikely.

Hang Seng, Daily

Sentiment on shares in general has stayed fairly positive in May as AI mania grips the tech sector and volatility remains low. The added positive for Chinese and Hong Konger shares is the likelihood that the PBoC will need to soften policy to some degree to support the economy’s recovery which as noted above seems to be less strong in Q2 so far.

20,000 exactly is a crucial psychological zone which has functioned as the main technical reference for some months. A move sharply away in either direction would probably need a strong catalyst; that might not come until next quarter. Based on TA alone, a new phase of late 2022’s uptrend would seem to be more likely than a new downtrend, but that depends on the news and monetary policy. January’s high around 22,800 might be the next important resistance.

Apart from the PBoC’s meeting on Monday, there’s no major news scheduled from China next week. Traders might focus on international stock markets and tech earnings.

If you want to learn more about what is moving the markets, join our monthly live analysis

and trading session this coming Monday. Register here.

The opinions in this article are personal to the writer. They do not reflect those of Exness or FX Empire.

This article was originally posted on FX Empire