Yahoo Finanza

Yahoo Finanza Consumer Pandemic Spending Behaviors Remarkably Uniform with Recovery Tracking for Early 2023

Counterintuitive spending patterns identified in 12.4 billion transactions across all income and credit tiers provide compelling insights for lenders and policymakers

Graph: YoY % Change in $ Spend, by Risk

Argus, a Verisk (NASDAQ: VRSK) business

WHITE PLAINS, N.Y., Nov. 15, 2021 (GLOBE NEWSWIRE) -- The COVID-19 pandemic caused consumers to spend significantly less year-over-year beginning in March 2020, and that pattern was remarkably consistent across all regions and demographics in the United States, according to a study of 12.4 billion consumer credit and debit transactions. The study, conducted by Argus and believed to be the largest of its kind, also found that consumer spending may not fully recover to pre-pandemic levels until early 2023.

To explore the impact of the pandemic on consumer spending, Argus, a Verisk (NASDAQ: VRSK) business, studied both credit and debit transactions across the wallets of approximately 20 million consumers, a representative sample of the overall credit-card-active population. The study spanned from January 2019 through December 2020, comparing monthly spend year-over-year to control for seasonality throughout the year. The study also evaluated credit and debit transactions of these same consumers through May 2021 to further understand spend recovery dynamics.

The COVID-19 pandemic caused consumers to spend significantly less year-over-year beginning in March 2020, but the remarkable finding was the consistency of that drop in spend across the country. The timing of changes to spending levels was the same regardless of consumer age, risk score, or geographic region. This was in stark contrast to previous economic downturns, where spending patterns differed by region and consumer profiles. Analysis of spending patterns since the 2020 pull-back also indicates that spending may not fully recover to pre-pandemic levels until early 2023.

“When the country shut down and so many retailers, restaurants, and bars closed their doors, consumers temporarily lost many of their usual spend outlets,” said Linda Turnbull, Associate Managing Director at Argus. “What is fascinating is that the timing was so consistent even though new COVID cases surged in different regions of the country and for different age groups at different times.”

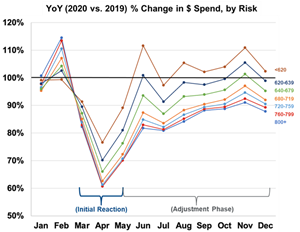

According to the study, overall consumer spending dropped on average 16% in March 2020 compared to March 2019. In April 2020, the year-over-year drop was more severe, at 38%. However, in May 2020, a spend recovery was already underway, with year-over-year spend down a significant but less severe 28% relative to 2019, a 10-point improvement over April.

“Unlike the 2008 recession, when spend dynamics differed materially across different local economies, the drop in spend due to the pandemic had the same timing in every single view of the data we analyzed, which is unprecedented,” said Turnbull. “However, the recovery has shown unexpected trends. For example, we have found that spend among the highest-risk consumers is recovering fastest. Taken together, these findings have significant implications for how lenders and policy-makers should develop strategy.”

Data Show Counterintuitive Patterns for Essential vs. Non-essential Spend

The study also explored how consumers managed essential spend versus non-essential spend during the pandemic. Essential spend included categories like food, medications, gas, and groceries. Non-essential spend examples included airline travel, clothing stores, and furniture stores. In all, there were 877 different spend categories classified as either essential or non-essential. Not surprisingly, both essential spend and non-essential spend dropped last year. By April 2020, non-essential spend dropped nearly twice as much year-over-year (47% on average) as essential spend (down 25%). Both spend types began their recovery in May 2020, with essential spend recovering significantly faster than non-essential spend. Across all age and risk tiers, essential spending had more-or-less fully recovered by the end of 2020. However, non-essential spend has still not recovered for many segments of the population.

Interestingly, non-essential spend recovery has been faster for higher-risk consumers, i.e., those with lower credit scores. This is counterintuitive; the conventional wisdom is that lower-risk consumers generally have more disposable income and more available credit with which to spend.

“It came as a surprise to see higher-risk consumers return faster to pre-pandemic spending levels,” said Turnbull. “We believe this may be explained in part by the differences in the type of non-essential spend lower-risk consumers make versus higher-risk consumers.”

For example, travel spend comprised almost 24% of pre-pandemic spend for lower-risk consumers, but only 17% of non-essential spend for higher-risk consumers. Travel has been slower to recover than other forms of non-essential spend, such as restaurants and taverns. Another possible driver may be differences in the number of transactions and the dollar amount of spend between the two groups.

“Higher-risk consumers generally have less disposable funds available and so spend less on average on non-essentials. For example, it’s possible that going out for dinner even one extra time each month can bring higher-risk consumers back to their pre-pandemic spending levels. This is less likely with lower-risk consumers, who spent considerably more—and more often—on non-essentials pre-pandemic. This is an interesting open question that we look forward to exploring further,” continued Turnbull.

Consumer Spend Recovery Analysis Vital to Understanding the Consumer Condition

The study also explored the spend recovery dynamic.

“What amazed us was how quickly the recovery began,” said Lisa Bonalle-Hannan, President of Verisk Financial. “We were impressed by the speed with which consumers and merchants alike adjusted to the pandemic environment, with more online shopping, expanded use of mobile and other contactless payment methods, and increased convenience options, such as curbside pickup to enable safer transactions. However, that recovery process is not complete.”

Argus developed several forecasting models for non-essential spend to estimate when spend would achieve full recovery. The more conservative models estimated that spending among the lowest-risk consumers—those anticipated to be the last to reach their pre-pandemic spend levels—would not fully recover until early 2023.

“Forecasting consumer spend is a difficult challenge, particularly when the environment continues to be volatile,” Bonalle-Hannan said. “With the delta variant still surging across the country, the pandemic is far from over. But it is important to distinguish between recovery from the pandemic and spend recovery. While the pandemic still impacts our daily lives, we feel confident that spending is well on its way to full health. Importantly, our study found that non-essential spend is the key to total recovery. Therefore, that’s a key indicator we continue to track closely.”

“This analysis is hugely important to lenders, policymakers and consumers alike,” concluded Bonalle-Hannan. “The insights we can provide into how consumers spend and what drives those behaviors at the individual consumer level, and across the wallet, are critical for both lenders and policymakers to better understand the consumer condition in these difficult times. This study also suggests several ways in which issuers can engage more effectively with their customers and prospects. With greater understanding and deeper insights, lenders will be better positioned to help consumers across the country weather the unprecedented storm of the COVID pandemic.”

For more information about this Argus study, please visit argusinformation.com/contact.

About Verisk Financial Argus

Argus, a Verisk (NASDAQ: VRSK) business, is a leading provider of intelligence, decision support solutions, and advisory services to financial institutions across the global commerce ecosystem. Our clients include more than 50 top US, Canadian, and other international financial organizations, regulators, payment providers, merchants, and media. Argus is the leading source of segment-level portfolio management benchmarking data, analytics, models, and advisory services. We maximize value delivery to clients by combining proprietary data sets, cutting-edge software and analytic tools, domain expertise, and our unique results-oriented approach. Customers worldwide use our services for tailored data management solutions that include business intelligence platforms, profile views, mobile data solutions, enterprise database services, and fraud risk scoring algorithms for marketing, fraud, and risk mitigation. To learn more, visit argusinformation.com.

Attachment

CONTACT: Kevin Sugarman GlobalFluency 408.677.5311 ksugarman@globalfluency.com