Yahoo Finanza

Yahoo Finanza C3.ai Is Undervalued, but Will Face Profitability Pressures

C3.ai Inc. (NYSE:AI) is operationally undervalued by the market, primarily because it has stronger competitors like Palantir Technologies Inc. (NYSE:PLTR). I believe investors will have reasonable long-term returns if they invest in the stock now, but I do not expect these to be higher than Palantir's.

As such, I believe investors will want to consider the similar risk-reward profile of both companies and then assess the higher growth prospects of Palantir. Because both investments carry somewhat higher risk than other established players, my own preference is to choose the allocation that may provide a significant amount of outsized growth as a result.

Company and AI market analysis

C3.ai is one of the lesser-known but still important companies working in the artificial intelligence industry. It specializes in enterprise AI, with notable competitors in the space, including Salesforce (NYSE:CRM) and Palantir. Its flagship product, the C3 AI Suite, offers the development, deployment and operation of AI applications, driving efficiency and cost-effectiveness with a focus on enterprise data management.

The company offers a crucial product and service set, but I am unsure how unique its offering is. Hence, I believe it may fall prey to finding itself both easily replicated and potentially outcompeted by more established and profitable players, but also by the newer companies that potentially have some advantage already in capability, like Palantir. C3.ai's strategic partnerships are strong and include Microsoft (NASDAQ:MSFT) and Adobe (NASDAQ:ADBE), but these partnerships are becoming increasingly common for enterprise AI companies and are nothing particularly special, in my opinion.

That being said, the executive leadership team is formidable, with Chairman and CEO Thomas M. Siebel having founded Siebel Systems, which merged with Oracle (NYSE:ORCL) in 2006. That extensive history in application software sets the stage with a veteran-level consciousness in applying time-tested lessons to these new burgeoning AI tools. I do not underestimate Siebel's experience and accolades, but I wonder how he will keep C3.ai competitive at a time when AI is literally the most popular business sector in the world. It seems probable to me that even strong companies, which are large and have hierarchies of executives, each with decades of technology knowledge, could get overpowered by other companies that simply get lucky in mass-scale adoption. For example, Salesforce is a company that seems to have quite crucially cornered the retail AI market early enough to potentially solidify itself as the main provider. Even if C3.ai can provide tools that are better and more comprehensive than Salesforce, the idea that it will get back the portion of the market that Salesforce seems to have already captured appears thin to me.

There is also Palantir, which I believe will outcompete C3.ai in U.S. defense work. C3.ai has contracts with the U.S. Department of Defense, the Defense Innovation Unit and the U.S. Air Force, and it is part of the Joint Artificial Intelligence Center project. This raises concern over how these AI technologies will be used and whether C3.ai will be pulled in directions that perhaps conflict with its corporate customers for the sake of national and international defense during wartime.

My own perspective is that even in the case of C3.ai favoring its government defense obligations to its corporate interests, Palantir offers the management of complexity, security and compliance, which outcompetes C3.ai in the defense sector at this time. Palantir was founded six years earlier, so I believe it has some advantage in operations simply due to time in the field.

Financial analysis

C3.ai is not profitable yet, and I believe this provides investors with somewhat of an opportunity because it is usually when companies begin to report stable earnings that the wider stock market begins to take notice and push up the company's valuation. However, it also comes with a set of risks that make me skeptical about allocating significantly to the stock.

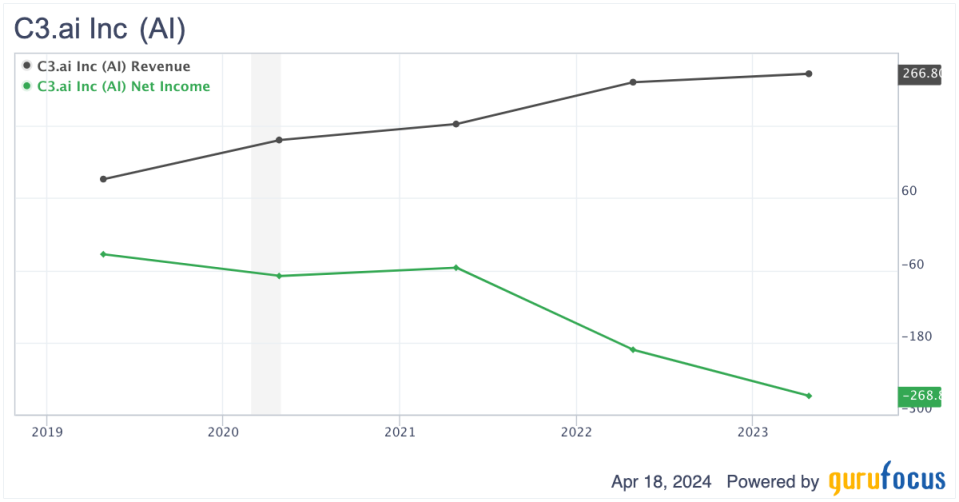

In many respects, the capital structure has to be admired because the company carries no typical debt, although it does have moderate lease obligations and other liabilities contributing to its equity-to-asset ratio of 0.84. This is high, and I believe it shows strong financial management that should translate into a stable bottom line in due course. Additionally, the company's operations with a portfolio of high-status clients, including government contracts, show signs of potentially stable future earnings. The good news is that C3.ai's revenue is growing at a healthy rate and it is quite understandable that it is investing heavily in research and development and its operating costs, as well as its cost of goods sold, are increasing quickly alongside its revenue. However, I believe C3.ai needs to take more stringent efficiency measures to create lasting profitability. What does not help is that C3.ai's gross margin of 59% has been decreasing, while Palantir's 81% margin has been increasing. The unfortunate reality right now is that while C3.ai's revenue is increasing fast, so is its net loss.

C3.ai has a roughly $2.50 billion market cap, while Palantir has a $47 billion market cap. Therefore, it is not unreasonable to say that C3.ai has a lot of catching up to do. Considering the problem is as immediate as the gross margin for C3.ai, it likely has higher purchase costs for product and service development because it is purchasing at a lower scale. In addition, it does not have the same full-stack AI and data services that Palantir has, likely driving up its cost of goods sold due to fewer in-house development capabilities.

Value analysis

Based on my analysis, it is not surprising that Palantir trades at higher valuation multiples than C3.ai. We can see evidence here of the efficient market hypothesis at work. To clarify, my own position is the markets are efficient, but evidently not totally efficient. I also have seen evidence that the smaller the company, the larger the inefficiency is likely to be if it occurs.

C3.ai is a mid-cap stock, while Palantir is a large-cap stock, so any value opportunities here are unlikely to be significant. However, C3.ai undoubtedly offers a better valuation to Palantir at this time, primarily a result of the fact that investors at large have begun to notice the long-term high value of Palantir as a U.S. defense and corporate asset and a company vital in harnessing AI for data management. I believe the market operationally undervalues C3.ai, and so its price reflects this. Consider its price-sales ratio of 8.13 versus Palantir's price-sales ratio of 21.90. As I mentioned above, the market's lower favor of C3.ai is well justified by Palantir's more comprehensive capabilities and financing power.

Additionally, Palantir offers better future growth prospects assessed on consensus by analysts. Therefore, I do not believe the most astute question here when analyzing the valuation of C3.ai or Palantir is whether they are selling below fair value, but rather whether the valuation is reasonable enough to justify the growth. In my opinion, Palantir offers much better future growth prospects and operational value, so the premium is worth it. I admit that Palantir could be selling slightly cheaper and I believe it will see a small correction soon. But even if bought at this time, I believe Palantir is likely to significantly outperform C3.ai over the next 10 years.

Risk analysis

As mentioned previously, C3.ai faces one of the same significant risks that I recently identified when researching Palantir. As it has a growing exposure to defense, intelligence and government sectors, it may find that during wartime, its resource allocation is conflicted between corporate interests and national and international security measures. It is my opinion that with the current global conflicts, which could escalate, C3.ai may be called upon with larger contracts and more definite demands from U.S. and NATO defense allies.

As such, it might find its development costs significantly redirected from corporate to defense interests for extended periods, significantly reducing its value to corporate clients during these periods and affecting or changing its reputation on return to times of peace. C3.ai's exposure to the military-industrial complex places shareholders in a nuanced position, in my opinion, and opens it up to certain risks related to shifts in its strategic focus that may not necessarily always be what is best for shareholder profits.

Summary

C3.ai is well-positioned to provide AI services to enterprises looking to become more efficient and automated, but it has fierce competition, most notably from Palantir. While its balance sheet is very strong, its net loss is growing alongside its revenue growth. Additionally, in times of war, C3.ai could find its operational focus significantly changes, affecting its utility to corporate clients and associated value when returning to times of peace.

Although the stock offers good value at this time, I believe investors are more likely to have higher total returns from an investment in Palantir over the long term.

This article first appeared on GuruFocus.