Yahoo Finanza

Yahoo Finanza Oracle Is Too Cheap

Oracle Corp. (NYSE:ORCL), a large-cap software-as-a-service and database storage/management company ($330 billion) is facing strong demand for it cloud-based services.

As a result, the company is set to generate large amounts of free cash flow and higher FCF margins. That could push the stock from 33% to 38% higher over the next year. This discussion will describe how that scenario will work out.

AI and cloud demand leading to higher growth

Corporations are moving to artificial intelligence-generated software products, and Oracle is selling the infrastructure (i.e., databases and data storage facilities) to do this in the cloud. Think of this as selling the shovels to gold miners during a gold rush.

Moreover, demand for its new AI generative software is skyrocketing. Larry Ellison, the chairman and chief technology officer, recently told shareholders on the March 11 earnings conference call that Oracle's cloud technology is not only just helping train large language models on which huge generative AI models are based. It has its own AI software. He gave an example of how this works in the health care industry:

This completely new application features a voice interface called the Clinical Digital Assistant (which) listens to a doctor's consultations with a patient and automatically generates prescriptions, doctor's orders, doctor's notes, then automatically updates the patient's electronic health records. The Clinical Digital Assistant's voice interface makes our new healthcare systems dramatically easier to use and saves hours of doctors' precious time every day, which now can be spent with patients rather than typing into a computer.

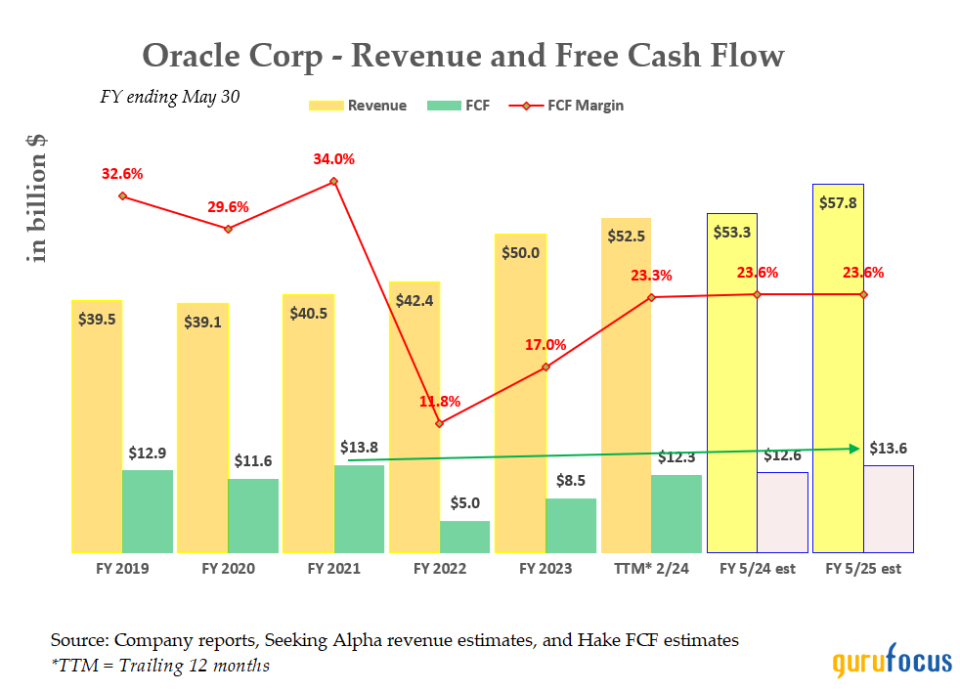

As a result, Oracle is set to post strong revenue in the future. This is despite lower growth rates on a year-over-year basis, presently digesting a large $28 billion June 2022 database company called Cerner.

For example, analysts now forecast revenue will rise 6.60% this fiscal year ending May 30 to $53.30 billion, but next year it will increase by 13.40% to $57.80 billion.

Moreover, this will lead to much higher free cash flow, which eventually could push the stock much higher.

Higher FCF is forecast

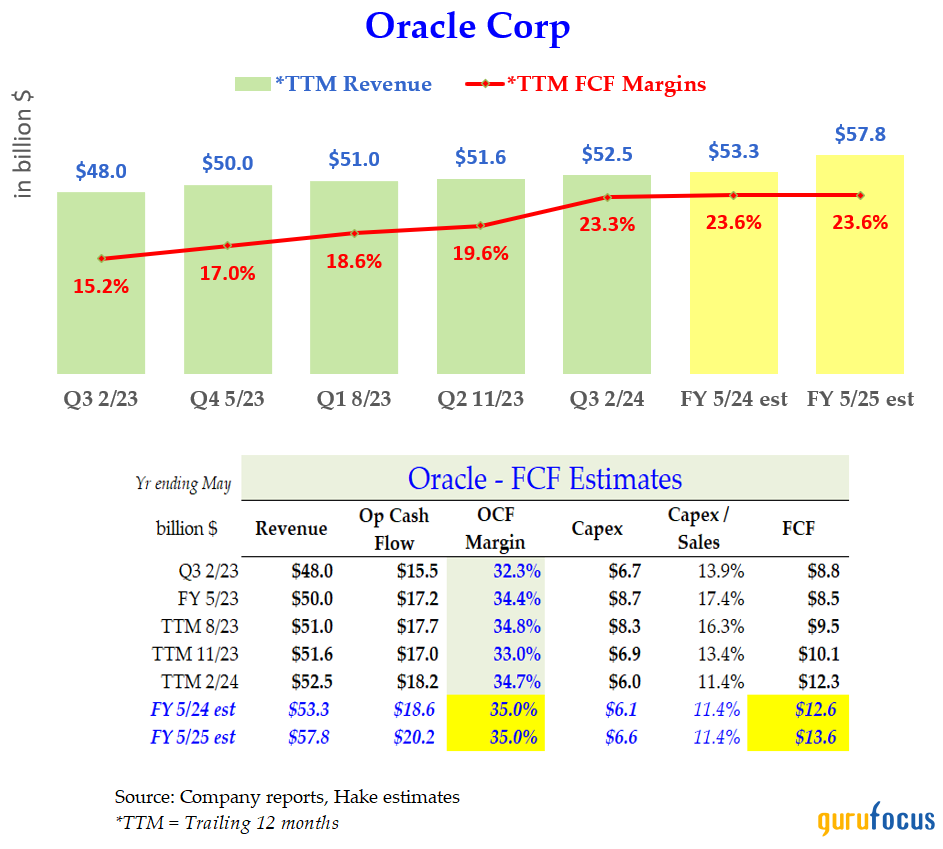

Oracle is one of the few companies that help investors by showing its calculations of trailing 12 months operating cash flow, capital expenditure and free cash flow levels. The table below shows it has consistently raised its FCF margins in the past six quarters on a trailing 12-month basis.

You can see these higher FCF margins are despite spending higher dollar amounts on capex. That is from the increasing demand to build out more cloud-based data facilities and its AI-related software.

So, for example, to forecast the next fiscal year I decided to use the same 35% operating cash flow margin of 35% as well as the same capex/revenue ratio of 11%. It is much more likely, however, that its OCF margin will be much higher going forward as the growth and lower expenses from the Cerner acquisition kick in.

The bottom line is that a very conservative estimate of the next fiscal year (ending May 2025) FCF is $13.60 billion, or a 24% FCF margin on sales of $57.80 billion.

Using that FCF estimate, the valuation for Oracle's stock could be much higher than today's price.

Target price

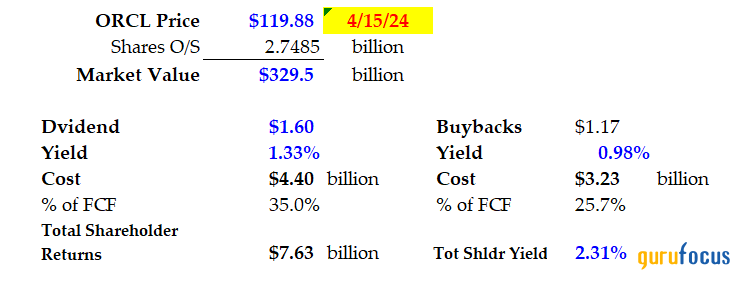

Right now, Oracle pays out a $1.60 dividend, which gives investors a 1.33% dividend yield. The table below shows this will only cost 35% of its free cash flow.

Moreover, the company spent $3.23 billion on buybacks in the trailing 12 months, which works out to a buyback yield of about 1%. So combined, the shareholder yield is 2.31%.

This also implies that if the company were to pay out 100% of its FCF next year, it would likely have about a 3.50% to 3.80% dividend yield. Moreover, based on investors' preference for dividends, the yield could drop to 3%.

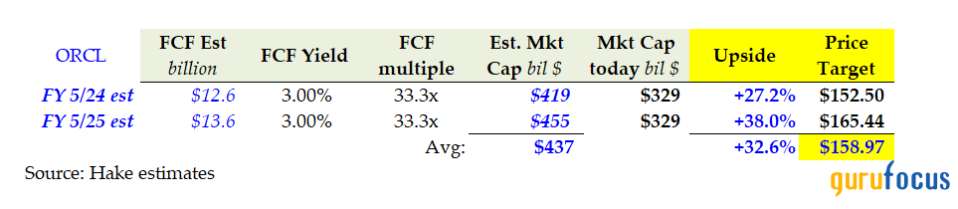

As a result, using a 3% FCF yield metric, the value of Oracle's stock would be as follows: divide its FCF by 3% to determine its prospective market capitalization. This can be seen in the table below.

It shows that, on average, Oracle would have a $437 billion market cap and possibly as high as $455 billion. That implies the target price will be between $152.50 and $165.44 per share, or 27% to 28 % higher. The average is $159 per share, or one-third higher.

Potential catalysts for a higher price

Analysts so far have much lower price targets. For example, AnaChart, a sell-side analyst tracking service shows the average price target of 28 Wall Street analysts is $140.28 per share. That is over 12% higher than today's price.

Analysts tend to be short-sighted on stocks with recent slower revenue growth. They often only react after high growth kicks in. However, I have shown the company is set to make significant FCF margins and good free cash flow, which could push the stock much higher.

The bottom line here is Oracle still looks too cheap now. This is especially the case if its cash flow margins come in much higher than expected. That is very likely given the strong demand for its AI-related cloud-based infrastructure and SaaS products.

Moreover, the company is likely to use much of that FCF to benefit shareholders. It can easily afford not only its existing dividend, which has stayed at the same level for five quarters now, but also its huge buyback program. Increases in any of these programs from higher FCF could act as a catalyst for Oracle's stock to rise by one-third to the $159 target price.

This article first appeared on GuruFocus.