Yahoo Finanza

Yahoo Finanza RTX Is Heading to a Healthy Correction After Outperforming the Competition

Shares of RTX Corp. (NYSE:RTX) have outperformed year to date, but it may be time for a healthy, short-timed correction or a lengthier stagnation until competitors catch up. The defense sector is likely to outperform the broader market due to global tailwinds, but RTX has turned slightly too expensive relative to its competitors after some of the company's 2023 fears started to fade too early, while some key growth blockings remain unresolved.

Stock performance

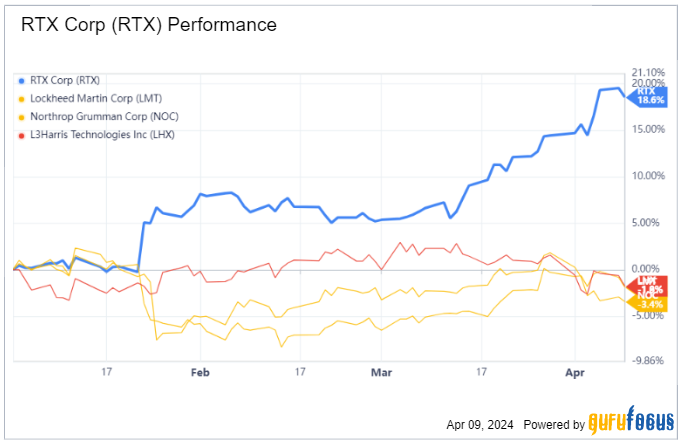

The stock has been outperforming the broader defense sector and its direct competitors, Lockheed Martin (NYSE:LMT), L3Harris (NYSE:LHX) and Northtrop Grumman (NYSE:NOC), by a wide margin. Multiple new price targets have been announced over the last couple of months that contributed in boosting the stock price, despite no real change or improvement in both fundamentals and key challenges the company faced in 2023 when it actually underperformed.

Barclays increased its target price for RTX from $75 to $90 on Jan. 30. Bank of America recategorized the stock from underperform to neutral and its target from $78 to $100 on Jan. 25. UBS Group upped its new target price to $96 from the previous $93 target on Jan. 24. On March 19, it was TD Cowen's turn to raise its outlook for the aerospace and defense company from $106 to $115 with an outperform rating. Lastly, based on data from MarketBeat.com, the stock has a neutral consensus rating with an average target price of $95.76. Interestingly, the stock is currently trading around $101, which means four of these five new targets are still below the current trading price.

As you can see in the above chart, the three competitors are essentially flat year to date, while RTX is up by approximately 18.60% after three months of trading. In this discussion, I will explain the reason for the outperformance and why it is paradoxically not the best defense stock to buy right now. Indeed, RTX ended 2023 down 16.60%, underperforming the S&P 500 by more than 40%.

Therefore, I believe the stock's outperformance this year is merely due to a catch-up effect after a year to forget for shareholders, fading fears without actually being resolved and target price hikes powering the stock momentum.

Business overview and challenges

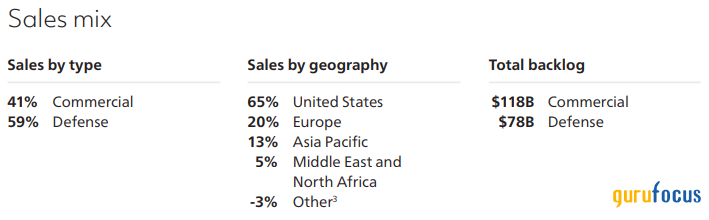

RTX is composed of four different businesses: Collins Aerospace, Pratt & Whitney, Raytheon Intelligence & Space and Raytheon Missiles & Defense.

Collins Aerospace focuses on the manufacturing of aerospace products for commercial, regional, corporate and military aircraft and is also a major supplier for international space programs. Pratt & Whitney designs and builds aircraft engines and gas turbines, while Raytheon Intelligence & Space specializes in communication, sensor systems, cyber and software solutions to governmental and commercial customers. Raytheon Missiles & Defense focuses on missiles and generally everything in relation to detecting and engaging threats.

RTX's Pratt & Whitney business discovered a risk of contamination in its powder coating, which is a material used to produce engine turbine discs. This contamination could cause several billion dollars in losses, severely impacting corporate earnings and free cash flow. Given the company has been an important dividend payer to shareholders for decades, any reduction of the dividend payments due to a decline in earnings could quickly initiate a panic spiral among investors - especially when you have alternatives in competitors like Lockheed Martin, L3Harris and Northtrop Grumman that all pay dividends and have similar business cases. Another key concern I have for the company, but applicable to the sector overall, is supply chain and shipping disruptions, as well as rising basic materials prices and labor costs. These disruptions and cost increases have impacted many business across the United States, and the defense sector is not immune.

Financials and valuation

Zooming in on the financials, particularly cash flow, RTX is expected to report disappointing free cash flow growth of 4.50% this year due to the issues I described. This is in stark contrast with 2023, when the company generated cash flow growth of 12%. The markets are forward looking: this year's disappointing figure was probably priced in last year when the stock declined 16.60%. The recent stock rally was powered by markets tabling a whopping 23% free cash flow growth. A lot has to go right for the company to reach that level of growth; high expectations mean the bar is really high and it is not my personal preference when initiating a buying position. Indeed, the company's free cash flow declined 2.60% in 2022 before recovering with 12% growth in 2023. It is expected to have mid-single-digit growth this year.

The high expectations for next year combined with the current high valuation makes an increase in my position undesirable, so I would prefer to wait for a better entry point.

Indeed, as you can see in the above chart, the stock is currently trading at 18.30 times last 12-month Ebitda as of April 8 (with valuation continuing to spike) while during the pre-Covid (2019) and post-Covid (2021-2023) periods, it was trading around 15. With an enterpise value-to-Ebitda multiple of 15, we would have a current stock price of around $85. A slight premium up to $90 would be acceptable given the sector tailwinds and possible good news on RTX's Pratt & Whitney business.

When considering competitors' valuations, we realize that RTX's current valuation may be unjustified. Lockheed Martin is trading at 12.30 times while L3Harris Technologies is at 15.30. Northtrop Grumman is currently trading at 20 times, but this is an anomaly due to a 50% decline in Ebitda last year as the stock was trading in a tight range between 2020 and 2023. The valuation of RTX, therefore, does seem slightly stretched in relation to the sector and the market may have gotten ahead of itself with the high growth tabled for 2025.

Factors that could invalidate my thesis

Because of its expensive valuation, its powder coating contamination that could delay operations and the political obstruction, namely in the U.S. Congress, I would not initiate a buying position at this stage. However, if you already own the stock as I do - I currently own it with an average purchase price of $87 with four positions ranging from $85 to $90, which is roughly where I currently value it for, in line with competitors - it makes sense to continue holding it if your time horizon is over at least two to three years.

On top of price, what I want to see before buying again is improving prospects on the existing operational issue at its core segment, Pratt & Whitney, a more detailed plan from management on supply chains and cost management and at least preliminary signs of a consensus between both parties in the U.S. Congress on bills in relation to Ukraine and Israel military or financial support. Given the intense geopolitical situation with the wars in Ukraine and Israel-Palestine, market tailwinds could support the stock price and buy the management team some time to solve the powder coating problem. Furthermore, interest rate cuts by the Fed this year and/or next year could support the current stark valuation, but this scenario remains hypothetical as the U.S. economy continues running strong and inflation shows some signs of rebound since the start of the year.

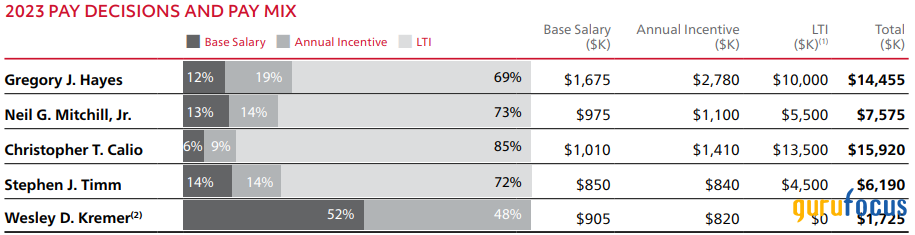

Last but not least, the strongest argument that convinced me to buy and hold for the long term is the existing management remuneration plan. As Charlie Munger famously declared, "Show me the incentive, and I will show you the outcome." Below you can see an extract of the incentives plan from the RTX 2024 Annual Proxy Statement.

Christopher Calio is the President and CEO and Gregory H. Hayes is the executive chairman. Respectively 94% and 88% of their pay is based on annual incentives and long-term incentives. These incentives are based on objective criteria such as financial growth, employee retention and energy emissions of the company. These incentives align the management's interests to the shareholders' as the fixed base salary range for the top two individuals is in a very low 6% to 12% range.

Bottom line

Depending on your time horizon, I would hold the stock for the longer term, because it is a well-established company with market tailwinds and an incentive plan based on the company's sustainable growth, which puts management's incentives in line with the shareholders'. However, I do feel that the stock got a bit ahead of itself in the first quarter and is trading at a premium to its current fair value, which I would currently estimate to be around $85 to $90 based on multiples historically applied to the stock and the sector. I would, therefore, wait for a correction to initiate a new position.

This article first appeared on GuruFocus.