Yahoo Finanza

Yahoo Finanza Vanguard Commentary: Building Resilient Portfolios Through Diversification

After a period of relative market calm, market dynamics in the last few years have called into question the viability of traditional allocation models like 60% stocks/40% bonds and the conventional roles of asset classes. Cash delivered record returns, bonds fell in tandem with stocks in 2022, and U.S. equities continue to outpace international securities. The speed at which the landscape changed, as central banks attacked inflation with higher interest rates, serves as a trong reminder of why investors need to resist the temptation to chase performance and why portfolio diversification remains as important as ever.

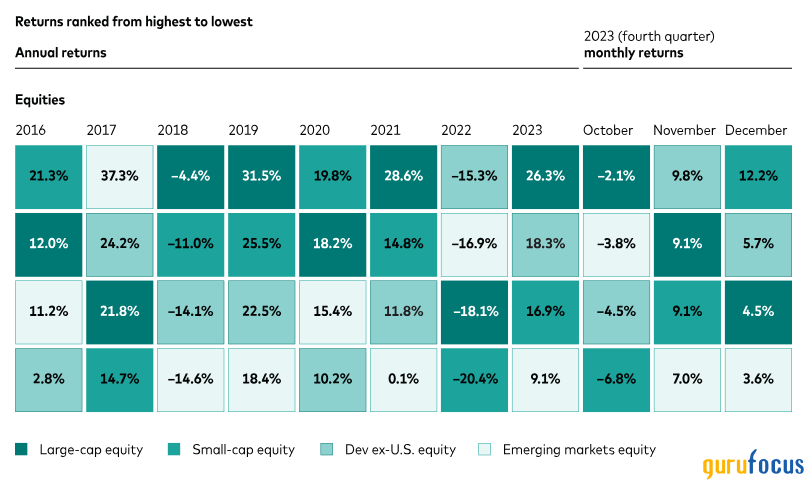

Equities

U.S. equities have contributed to much of the overall market performance since the global financial crisis in 20082009. The low interest rate environment, rising stock valuations, and high earnings in the U.S. allowed a broadly diversified U.S. stock portfolio to return almost twice as much as a comparable international portfolio over the past decade.

U.S. equities continue to be a strong performer, but the drivers of that outperformance over the last decade have likely sown the seeds for more muted performance over the coming one. With stretched valuations and a slowdown in earnings growth, we're forecasting annualized returns of 3.7%5.7% in the U.S. equity market over the next decade. Investors should be cautious with U.S. equities, considering the expensive valuations and lower expected growth. By comparison, we anticipate returns of 6.9%8.9% annualized over the next decade for international equities because of the multidimensional growth opportunities given lower volatility, cheaper valuations, and higher potential for growth.

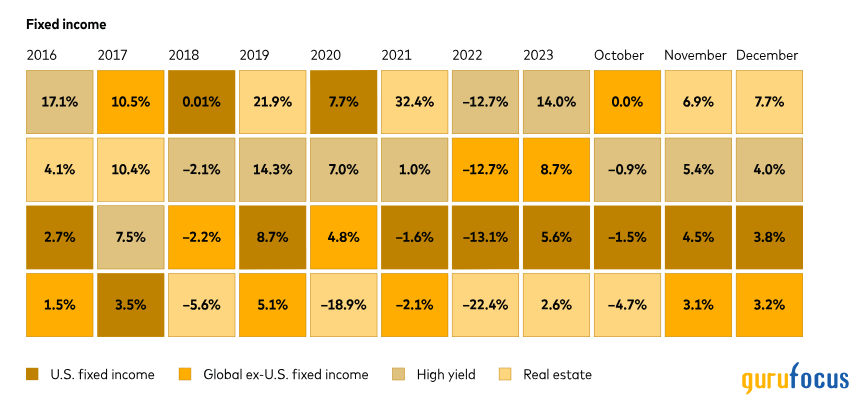

Fixed income

Historically, bonds have served as a stabilizer for a portfolio because there's usually less volatility risk in fixed income than in equities. Over the past decade or so, investors shied away from bonds in favor of cash and cash equivalents. But bonds and cash serve separate and distinct purposes. Over the long term, high-quality bond funds have tended to offer better diversification against stock volatility and higher yield potential than cash. While replacing bonds with cash may work in the short term, investors need to consider more than just yield if they want to design an all-weather portfolio.

Current economic conditions have made fixed income a more viable asset class that can grow over time and compound your returns for medium- to long-term savings needs. Global bond markets have repriced significantly over the last two years as interest rates increased, putting bond valuations close to fair. We expect both U.S. and international bonds to return a nominal annualized 3.9%4.9% over the next decade. While we expect similar returns for U.S. and international fixed income, it'll remain important to diversify because international bonds can mitigate overall volatility and improve portfolio outcomes through lower correlations.

Cash

Investors should think of cash as the tool to manage liquidity riskit can be a strategic allocation for day-to-day needs, for emergency savings, or for those with a very low risk tolerance. Cash should not be considered a substitute for stocks or bonds in any market environment, even in the current high interest rate environment, where investors have been able to get a real return on cash.

On the face of it, shifting your portfolio to cash seems like a good idea in this environment: There is no risk in cash and you're getting the same return you might from bondsfor now. But cash is limited in its ability to keep up with inflation and investing in cash means forgoing risk premium. Investors must also consider the durability of the yield, which is anchored to monetary policy. If central banks cut interest rates, the yield on cash decreases, and you'll miss out on the income you would have earned if you had maintained your target bond allocation.

The current economic and market environment is primed to tempt investors to consider forgoing their strategy in order to chase returns. But across and within asset classes, we can't account for everything, such as how an AI-led productivity boom or geopolitical events could affect returns. Market leadership is not guaranteed, and chasing returns can leave investors exposed to unnecessary volatility and risk. Our research shows that a balanced mix of diversified assets, combined with a disciplined, cost-conscious approach to investing, can help improve investors' chances of achieving their long-term investment goals, as long as they stay the course.

Notes: Sub-asset classes include large-capitalization equity as measured by the Standard & Poor's 500 Index, small-cap equity as measured by the Russell 2000 Index, developed ex-U.S. equity as measured by the FTSE Developed ex-North America Index, emerging markets equity as measured by the FTSE Emerging Markets Index, U.S. fixed income as measured by the Bloomberg U.S. Aggregate Bond Index, global ex-U.S. fixed income as measured by the Bloomberg Global Aggregate ex-U.S. Bond Index, high-yield fixed income as measured by the Bloomberg Global High Yield Bond Index, and real estate as measured by the FTSE/EPRA Nareit Developed REIT Index.

Sources: Vanguard and FactSet, as of December 31, 2023.

Past performance is no guarantee of future returns. The performance of an index is not an exact representation of any particular investment, as you cannot invest directly in an index.

Note:

All investing is subject to risk, including the possible loss of the money you invest.

Be aware that fluctuations in the financial markets and other factors may cause declines in the value of your account. There is no guarantee that any particular asset allocation or mix of funds will meet your investment objectives or provide you with a given level of income.

Diversification does not ensure a profit or protect against a loss.

Investments in bonds are subject to interest rate, credit, and inflation risk.

Investments in stocks or bonds issued by non-U.S. companies are subject to risks including country/regional risk and currency risk. These risks are especially high in emerging markets.

This article first appeared on GuruFocus.